Many aspiring investors imagine that entering the financial markets requires a massive chest of capital, a complex understanding of economic theory, or access to private wealth managers. This persistent myth functions as a significant psychological barrier, delaying or completely preventing individuals from beginning their wealth-building journey.

The reality of the modern financial landscape is dramatically different. Driven by technological innovation, intense brokerage competition, and regulatory shifts, the barriers to entry have effectively collapsed. Today, it is entirely feasible to plant the seeds of your financial future with a modest budget—even as little as $5, $10, or $50.

The critical factor in wealth accumulation is not the size of your initial deposit; rather, it is the consistency of your contributions, the optimization of your strategy, and the time horizon you allow your assets to grow. If you’ve ever wondered how to start investing with little money, this comprehensive guide will demystify low-capital investing, providing a transparent, step-by-step roadmap for beginners to maximize small sums of money and build a secure, stable financial future.

Key Takeaways

- You don’t need thousands of dollars to start investing.

- Starting early is usually more important than starting with a large amount.

- Consistent investing and compound growth can help build wealth over time.

- Low-cost index ETFs, fractional shares, and robo-advisors make investing accessible.

- Always build an emergency fund and pay off high-interest debt before investing aggressively.

- Focus on long-term investing instead of trying to time the market.

Section 1: Why Start Investing, Even with Small Amounts?

Waiting until you have “enough money” to invest is a fundamental strategic mistake. In personal finance, time is a far more powerful multiplier than capital. Understanding the mathematical and behavioral advantages of starting small can provide the necessary motivation to take immediate action.

The Power of Compounding: The Eighth Wonder of the World

Compound growth is one of the most powerful forces in investing — your returns generate their own returns over time, and the effect becomes dramatic over a decade or more. For the full mechanics of how this works, our guide to how to start investing with $100 breaks it down in more depth. Here’s a different way to see the same principle in action:

- Sarah starts investing $50 a month at age 22. Assuming an average annual return of 8%, by the time she reaches age 62, her total contributions of $24,000 will have grown to over $175,000.

- David waits until he is 32 to start, but he invests $100 a month—double Sarah’s amount. By age 62, despite contributing $36,000 of his own money, his portfolio will only be worth roughly $150,000.

Sarah invested less total capital but ended up with more wealth simply because she gave her money an extra ten years to compound. This highlights why entering the market early with small amounts vastly outperforms entering late with larger sums.

Achieving Long-Term Financial Goals

Whether your objective is saving a down payment for a home, funding a child’s future education, or achieving complete financial independence, traditional savings accounts are structurally unsuited for long-term wealth accumulation. Because traditional banks offer interest rates that rarely keep pace with the rate of inflation, leaving your capital in cash means your purchasing power is actively eroding over time.

Investing serves as an economic shield and an engine for growth. By allocating small amounts of capital toward productive assets like stocks, bonds, or real estate trusts, you give your money the opportunity to outpace inflation and meaningfully fund your future milestones.

Building Bulletproof Financial Habits

The behavioral benefits of low-capital investing are just as critical as the mathematical ones. When you begin investing with limited funds, the stakes are low. If you make a mistake or experience a market downturn, the financial impact is minimal, providing a low-risk environment to learn the mechanics of the market.

More importantly, automated small-scale investing transforms the concept of saving from a conscious, painful monthly chore into an automatic, baseline financial habit. It forces you to adopt the golden rule of personal finance: Pay yourself first. Instead of investing what is left over after your monthly spending, you learn to live on what is left over after your investments are automatically deducted.

Section 2: Essential Pre-Investment Steps

Before exposing any amount of money to market volatility, you must establish a secure financial foundation. Skipping these foundational steps can force you into a position where you are required to liquidate your investments at an inappropriate time, turning temporary market fluctuations into permanent financial losses.

1. Define Your Financial Goals and Timeline

Every investment strategy must be reverse-engineered from a specific objective. Your goals dictate your asset allocation and your tolerance for volatility. Financial goals are generally categorized into three distinct time horizons:

- Short-Term Goals (0–3 Years): Saving for a vacation, a wedding, or a down payment on a car. This capital should remain highly liquid and protected from market drops (e.g., in high-yield savings accounts or short-term certificates of deposit).

- Medium-Term Goals (3–7 Years): Purchasing a home or starting a business. This allows for a balanced approach combining conservative equities and fixed-income assets.

- Long-Term Goals (7+ Years): Retirement or building generational wealth. Because you have time to recover from cyclical market recessions, this capital can be aggressively positioned in growth equities.

2. Build an Inviolable Emergency Fund

An emergency fund is your economic safety net. Without it, a sudden medical bill, a car breakdown, or an unexpected job loss could force you to sell your investments during a market downturn, locking in losses.

Before investing actively, aim to accumulate three to six months’ worth of baseline living expenses. Keep this money separated from your everyday checking account. It should be parked in a vehicle that offers safety and quick accessibility while still earning a competitive return, such as a High-Yield Savings Account (HYSA).

3. Honestly Assess Your Psychological Risk Tolerance

Risk tolerance is a combination of two factors: your financial capacity to take risk (determined by your timeline and income) and your psychological willingness to tolerate risk.

Ask yourself honestly: If your $500 investment temporarily dropped in value to $350 during a market correction, how would you respond? If your instinct would be to panic and withdraw the remaining cash to prevent further losses, your portfolio is likely too aggressive. Understanding your psychological boundaries early prevents you from making emotionally destructive trading decisions later.

4. Eliminate High-Interest Consumer Debt

Not all debt is created equal, but high-interest debt—such as credit card balances or high-rate personal loans—is an absolute wealth killer. The average interest rate on a standard credit card often hovers between 15% and 25%.

Mathematically, it is virtually impossible to find an investment that consistently and reliably yields a 20% annual return. Therefore, if you are paying 20% interest on a credit card debt while trying to earn 8% in the stock market, you are losing money on net. Prioritize an aggressive debt-repayment strategy (such as the debt snowball or debt avalanche method) before redirecting your surplus capital into investment vehicles. Before investing heavily, it’s often worth creating a financial plan and paying off expensive debt first. Our financial blueprint guide explains how to prioritize these steps.

Section 3: Accessible Investment Avenues for Low Capital

The democratization of fintech has resulted in an array of investment vehicles explicitly designed to accommodate micro-contributions and low minimum balances.

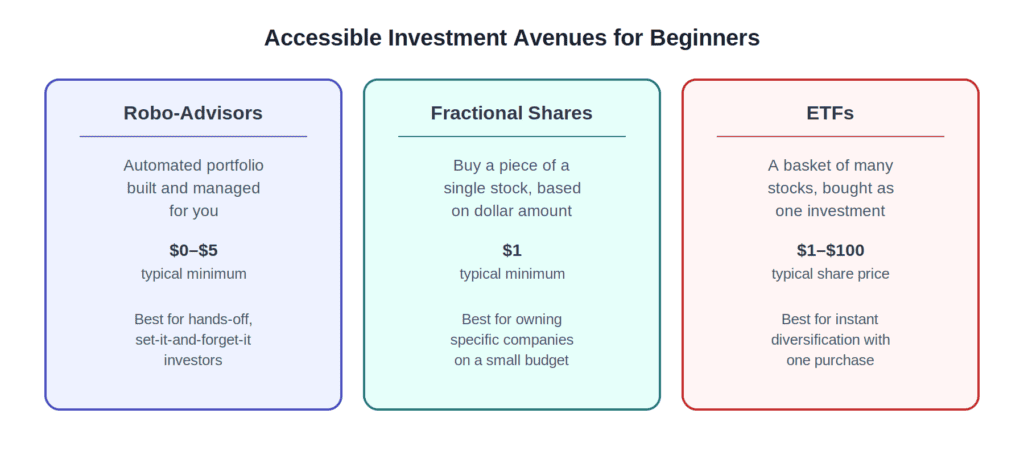

Robo-Advisors: Hands-Off Automation

Robo-advisors are digital platforms that use automated algorithms to build and manage an investment portfolio tailored entirely to your goals and risk tolerance. When you sign up, you complete a brief questionnaire regarding your timelines and risk comfort. The platform then automatically allocates your funds across a diversified selection of low-cost exchange-traded funds (ETFs) and periodically rebalances the portfolio to maintain that ideal mix.

- The Low-Capital Advantage: Many leading robo-advisors feature an account minimum of $0 or $5, making them incredibly accessible.

- Who They Are For: They are ideal for “set-it-and-forget-it” investors who prefer a fully hands-off approach to portfolio management without paying the high advisory fees associated with traditional human wealth managers.

Fractional Shares: Piece-by-Piece Ownership

In the past, to buy a stock, you had to purchase at least one full share. If a single share of a massive technology giant or an elite e-commerce platform cost $3,000, a beginner with $50 was entirely locked out of owning that company.

The introduction of fractional shares changed everything. Today, major modern brokerages allow you to purchase fractions of individual stocks or ETFs based on a specific dollar amount rather than a share volume.

If you want to allocate $10 to an expensive stock, the brokerage will simply credit your account with the corresponding percentage (e.g., 0.003%) of a share. This completely levels the playing field, allowing low-capital investors to construct custom portfolios of the world’s most successful companies.

Exchange-Traded Funds (ETFs): Instant Diversification

An Exchange-Traded Fund is essentially a basket of underlying securities (stocks, bonds, or commodities) that trades on a standard stock exchange exactly like an individual share. Instead of buying a single stock and tying your financial fate to one company, buying an ETF allows you to instantly spread your money across hundreds or thousands of companies simultaneously.

For example, an S&P 500 index ETF purchases fractional pieces of the 500 largest publicly traded corporations in the United States. If one company in the index experiences a bad year or files for bankruptcy, the remaining 499 companies help insulate your overall investment from disaster. Many highly diversified ETFs trade at share prices under $100, and when paired with a brokerage that supports fractional shares, you can buy into them for as little as $1.

Mutual Funds: Indexing with Caution

Like ETFs, mutual funds bundle individual securities to provide instant diversification. However, traditional, actively managed mutual funds often carry high initial investment minimums ranging from $1,000 to $3,000, along with higher management expense ratios.

For the low-capital investor, the exception lies in target-date mutual funds or broad-market index funds offered directly through retirement platforms. Some mutual funds have minimum investment requirements, while others—particularly those available through employer retirement plans or certain brokerages—allow investors to start with much smaller amounts.

High-Yield Savings Accounts (HYSAs) and CDs

While HYSAs and Certificates of Deposit (CDs) do not offer the explosive long-term growth potential of equities, they are vital components of a complete financial plan. Online banks often offer higher interest rates than traditional savings accounts, although rates change over time.

Because these accounts are protected by government deposit insurance, they carry zero risk of capital loss. They are the perfect, low-barrier vehicle for housing your emergency fund or accumulating the initial cash reserves you intend to transition into the market later.

Employer-Sponsored Retirement Plans: The Ultimate Catalyst

If your employer offers a workplace retirement plan—such as a 401(k) or 403(b)—and features an institutional company match, this should always be your very first investment destination. A company match means that for every dollar you contribute out of your paycheck, your employer contributes an equal amount up to a specific percentage threshold.

An employer match can provide an immediate return on your retirement contributions, making it one of the most valuable employee benefits available. Furthermore, because these contributions are deducted automatically from your pre-tax income, you never see the money enter your checking account, removing the temptation to spend it. If you’re unsure how retirement investing fits into a broader strategy, our beginner’s guide to stock market investing covers the fundamentals.

Section 4: Smart Strategies for Low-Capital Investors

Succeeding in the financial markets over the long run requires a strict adherence to proven investment frameworks rather than attempting to time market cycles.

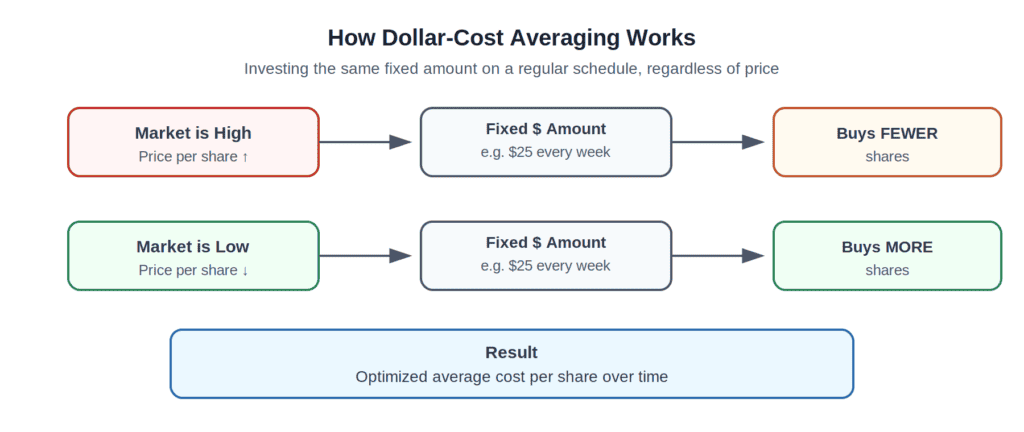

Master Dollar-Cost Averaging (DCA)

Dollar-cost averaging is the practice of investing a fixed dollar amount into a specific asset on a consistent, recurring schedule (e.g., $25 every single Friday), regardless of whether the market is up, down, or moving sideways.

This removes the pressure of trying to time the market — you just keep showing up on schedule, regardless of what prices are doing that week. For a deeper walkthrough of this strategy, our beginner’s roadmap to investing with $100 covers it in more detail.

Ruthlessly Diversify to Mitigate Risk

Diversification — spreading your money across many companies and sectors instead of betting on one — protects you from any single company’s bad year taking down your whole portfolio. Our stock market basics guide covers this in more depth, but the short version for a low-capital investor: a broad-market index fund gives you this protection automatically, in one purchase.

Commit to an Extended, Unwavering Timeline

The stock market is a highly chaotic environment in the short term. It reacts wildly to daily news cycles, geopolitical events, and emotional investor sentiment. However, historical data reveals that over long multi-decade horizons, broad equity markets have consistently trended upward.

Avoid the destructive habit of opening your investing app daily to analyze minor paper fluctuations. True investing is a marathon, not day-trading. Maintain a long-term perspective, trusting your automated strategy to weather short-term volatility.

Commit to Continuous Financial Education

The most valuable asset you can ever invest in is your own mind. The financial landscape is dynamic, with new platforms, rules, and economic conditions emerging regularly. Dedicate time to reading foundational books on personal finance, following reputable, non-sensationalist financial journalists, and understanding the core fundamentals of the assets you own. The more knowledge you acquire, the less vulnerable you will be to market hype, fear-mongering, and predatory investment schemes.

Eliminate Emotion from the Equation

Fear and greed are the two primary enemies of investment success. Greed drives individuals to chase speculative, high-risk assets at the peak of their valuation, while fear drives them to panic-sell their high-quality assets at the absolute bottom of a correction.

To achieve long-term success, you must intentionally decouple your emotions from your portfolio. Establish a clear plan, automate your system, and view market downturns not as disasters, but as rare opportunities to acquire high-value assets at a significant discount.

Conclusion: Your Journey Begins Now

The historical barrier of needing a fortune to build a fortune is officially dead. Through the tactical deployment of robo-advisors, fractional shares, index ETFs, and automated dollar-cost averaging, anyone can successfully construct a high-performing investment portfolio utilizing small, consistent amounts of capital.

Do not allow the illusion of “not enough money” to keep you on the financial sidelines. The absolute most critical step in the wealth-creation process is simply taking the very first one. Start exactly where you are today with whatever amount you can afford, stay disciplined, and let the relentless power of compounding transform your small contributions into long-term financial freedom.

Take the First Step Today

You don’t need to wait until you have thousands of dollars to begin investing. Open a brokerage account, automate a small monthly contribution, and focus on building consistent habits rather than chasing quick returns. Even modest investments made regularly can grow significantly over time.

FAQs: Beginner Investment with Low Capital

Q1: Can I really build substantial wealth starting with just $5 or $10?

A1: Absolutely. While a single $5 investment won’t fund your retirement, making a habit of investing $5 or $10 regularly (weekly or monthly) activates the power of compounding. Over a multi-decade timeline, those consistent micro-contributions grow exponentially, building a substantial financial base that you can scale up as your career earnings grow.

Q2: Is low-capital investing safe from heavy losses?

A2: All market investing involves some degree of risk, and your portfolio’s value will naturally fluctuate. However, you can significantly mitigate this risk by avoiding speculative individual stocks and focusing your capital on broadly diversified index ETFs or robo-advisor portfolios. Over long periods, a diversified approach is highly resilient.

Q3: Do I need a professional stockbroker or a degree in finance?

A3: No. Modern intuitive apps and robo-advisors handle all the underlying technical mechanics of trading and rebalancing for you. By focusing on broad index funds, you don’t need to analyze individual corporate balance sheets or follow complex market charts to succeed.

Q4: Should I invest my money or focus on a standard savings account?

A4: Both serve distinct purposes. Saving is for short-term stability and emergencies, ensuring your money is 100% safe and liquid. Investing is for long-term growth, accepting some short-term price fluctuations in exchange for returns that outpace inflation over time.

Q5: How often should I check my portfolio’s performance?

A5: Checking your account daily or weekly usually leads to unnecessary stress and emotional overreactions. For a long-term, low-capital investor, reviewing your portfolio once a quarter or twice a year is more than sufficient to ensure your automated contributions are processing correctly and your asset allocation remains aligned with your goals.

Investment Disclaimer

This article is for educational and informational purposes only and should not be considered personalized financial or investment advice. Investment values can rise and fall, and past performance does not guarantee future results. Consider consulting a qualified financial professional before making investment decisions.