Financial journaling sounds simple, almost too simple — but it addresses a particular kind of exhaustion that has nothing to do with being physically tired. It’s the kind that comes from carrying too many money worries at once — the bill you keep forgetting to pay, the vague anxiety about your savings, the purchase you’re still quietly regretting. It sits behind your eyes and follows you to bed.

Most of us know that feeling well. And most of us try to outrun it — avoiding our bank statements, distracting ourselves, hoping that if we don’t look directly at it, the mental noise around money will quiet down on its own.

It usually doesn’t.

What actually works — and what financial psychologists have been quietly confirming for years — is financial journaling. Not a complicated spreadsheet system, not a budgeting app with twelve categories. Just you, a page, and your honest thoughts about money.

This guide walks through exactly how to start a financial journaling practice, what to write, and why it works — in a way that fits real financial life, not an idealized version of it.

Why Financial Journaling Works — And Why Your Money Decisions Need It

Before the how, it’s worth understanding the why. When you understand what writing about money actually does to your decision-making, you’re far more likely to stick with it.

Here’s what happens when you put your financial thoughts on paper:

1. You externalize what’s internal. Money worries trapped in your head tend to loop — the same anxiety about a balance, the same regret about a purchase, the same vague dread about “not having enough,” often getting louder and more distorted with each pass. Writing pulls those thoughts out of the loop and pins them to the page. Once they’re external, you can actually look at them, evaluate them, and respond with a clearer head instead of just feeling them on repeat.

2. You activate a different part of your brain for financial decisions. Decades of research on expressive writing show that people who process emotionally difficult experiences on paper — including financial stress — report better mood, lower anxiety, and clearer decision-making afterward. Writing engages the rational, reasoning part of your brain, which helps quiet the panic response that often drives impulsive money decisions.

3. You create distance from financial emotions. There’s a concept in psychology called cognitive defusion — seeing your thoughts as thoughts rather than facts. Financial journaling naturally creates that distance. When you write “I feel like I’ll never get out of debt,” you’re no longer drowning in that feeling — you’re observing it. That shift, however small, changes how you respond to the actual numbers.

4. You build financial self-awareness over time. This is the long game, and it’s worth playing. When you journal about money regularly, patterns emerge. You notice what triggers your impulse spending. You notice the financial thoughts that keep recurring. You notice how your relationship with a specific debt or goal shifts week by week. That kind of self-knowledge is the foundation of almost every meaningful financial change.

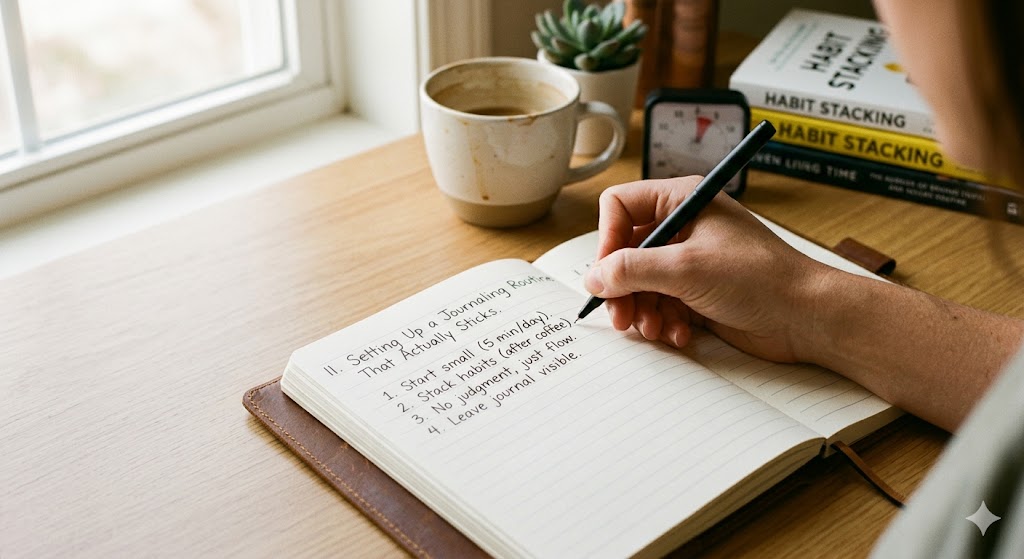

Setting Up a Financial Journaling Routine That Actually Sticks

The most common reason people abandon financial journaling isn’t lack of motivation. It’s lack of structure. They start with big ambitions, skip a few days, feel behind, and quietly stop.

A routine that actually holds up looks smaller than you’d expect:

Keep it to 5 to 10 minutes. This isn’t about writing pages. A few honest sentences about your financial state of mind is enough to get the benefit.

Pick a consistent trigger. Right after checking your bank balance, right before bed, right after a money-related conversation — tying it to an existing habit makes it far more likely to stick than relying on remembering to do it.

Don’t aim for perfect prose. Bullet points, fragments, half-finished thoughts — all fine. The goal is processing, not writing something polished.

What to Actually Write About

If a blank page feels intimidating, a few reliable prompts to start with:

After a financial decision (good or bad): What was I feeling right before I made this choice? Was I stressed, bored, anxious, excited? What was actually driving the decision?

During a stressful money moment: What specifically am I afraid will happen? Is that fear realistic, or is it bigger than the actual situation?

Once a week, a quick check-in: What’s one financial thing that went well this week? What’s one thing I’m avoiding looking at?

When you notice a recurring money worry: Is this thought based on a real number I’ve checked recently, or is it a vague feeling I haven’t actually verified?

That last one is particularly powerful — a huge amount of financial anxiety is based on numbers people haven’t actually looked at in weeks. Writing the question down often pushes you to go check, which replaces vague dread with an actual plan.

The Connection Between Financial Journaling and Better Decisions

This isn’t just a feel-good practice — it has a direct line to your actual money behavior.

Most impulse purchases and financial avoidance happen in a reactive emotional state, not a calm, deliberate one. When you build a habit of pausing to write about what you’re feeling around money, you create a gap between the trigger and the decision. That gap is where better choices happen.

It also surfaces patterns you’d otherwise miss. Maybe every financial journaling session in a particular week mentions stress about the same bill — that’s a clear signal something needs an actual plan, not just continued anxiety. Maybe a pattern of impulse spending always follows a stressful work day — now you know the trigger and can build a different response around it. This kind of pattern recognition is closely tied to the deeper wealth mindset shift that separates people who stay financially stuck from people who build real momentum.

If financial stress tends to show up alongside broader anxiety about money decisions, our piece on building financial resilience goes deeper into staying steady through those moments. And if you’re ready to pair the awareness from journaling with an actual plan, our weekend financial reset checklist is a strong next step.

Frequently Asked Questions

How is financial journaling different from regular budgeting? Budgeting tracks the numbers — what came in, what went out. Financial journaling tracks the thinking and emotion behind those numbers. They work best together: budgeting tells you what happened, journaling helps you understand why.

What if I don’t have anything specific to write about money? Start with a simple prompt: “How do I feel about my finances right now, in one honest sentence?” Even a short, vague answer is a starting point — the practice gets easier and more specific with repetition.

Can financial journaling actually help with debt or overspending? Indirectly, yes. It won’t pay down a balance directly, but by surfacing the emotional triggers behind spending and avoidance, it often leads to catching patterns early and making more deliberate decisions going forward.