Starting a small business is one of the most rewarding decisions a person can make — but it is also one of the most challenging. Many new businesses face significant setbacks in their first few years, often because of avoidable planning, financial, and operational mistakes, not because the entrepreneurs behind them lack passion or drive. The good news? Most of these small business pitfalls are predictable, and with the right knowledge and preparation, you can sidestep them entirely.

This guide walks you through the most common mistakes new entrepreneurs make — and more importantly, how to avoid them — from building a strong foundation and managing your finances to marketing your brand and scaling with intention. Whether you’re launching your first business or refining an existing one, avoiding these common pitfalls can save you time, money, and unnecessary frustration.

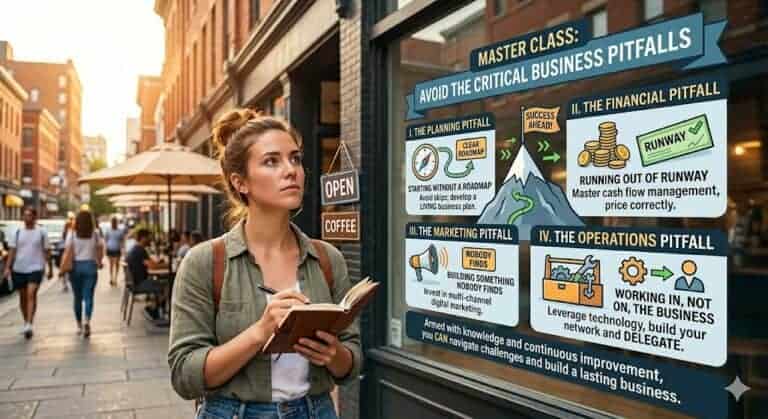

I. The Planning Pitfall: Starting Without a Clear Roadmap

One of the most common mistakes new entrepreneurs make is diving in without a proper business plan. Excitement and urgency can make planning feel like a delay — but skipping it is one of the fastest routes to failure.

Develop a Living Business Plan

A comprehensive business plan is not just a document for investors — it is your strategic roadmap. It forces you to think critically about your business model, define your target audience, set measurable goals, and anticipate obstacles before they arise. Your plan should include your mission and vision, a competitive market analysis, a clear value proposition, revenue and cost projections, and a go-to-market strategy. Crucially, treat this as a living document. Revisit and revise it as your business evolves, the market shifts, or new opportunities emerge.

Conduct Real Market Research

Many entrepreneurs fall in love with their idea without validating whether the market wants it. Thorough market research means identifying your ideal customer’s demographics, pain points, and purchasing behavior. It also means studying your competitors — understanding what they do well, where they fall short, and what gap you can fill uniquely. This research shapes your product, your messaging, and your positioning. It is not optional; it is the intelligence that separates thriving businesses from costly guesses.

Choose the Right Legal Structure

Your legal structure — whether a sole proprietorship, LLC, S-Corp, or C-Corp — has real consequences for liability, taxation, and administrative complexity. Many new entrepreneurs default to the simplest option without understanding the implications. Consult a legal or financial professional before registering your business. The right structure protects your personal assets, optimizes your tax position, and sets a sound foundation for future growth.

II. The Financial Pitfall: Running Out of Runway

Poor financial management is the silent killer of small businesses. Cash flow problems, underpricing, and inadequate funding are among the top reasons businesses shut their doors — even when the underlying idea is solid.

Secure Adequate and Realistic Funding

New entrepreneurs routinely underestimate how much capital they need. Startup costs often include equipment, licensing, inventory, website development, marketing, and at least six to twelve months of operating expenses before revenue becomes reliable. Explore all your options: bootstrapping, small business loans, SBA grants, crowdfunding, angel investors, or friends and family. Whatever route you choose, build in a financial buffer. Unexpected costs are common, so building a financial buffer into your budget is a wise precaution.

Master Cash Flow Management

Profit and cash flow are not the same thing. A business can be profitable on paper and still collapse because money is not arriving when bills are due. Create a detailed monthly budget and track every dollar in and out. Use accounting software like QuickBooks or Wave to gain real-time visibility into your finances. Review your cash flow statement weekly, especially in the early months. Knowing your numbers is not optional — it is survival.

Price Your Offering Correctly

Underpricing is one of the most common and damaging mistakes new entrepreneurs make, often driven by fear of rejection or a desire to compete on cost. Your pricing must cover your costs, reflect the value you deliver, and position your brand appropriately in the market. Research competitor pricing, understand your cost structure, and have the confidence to charge what your product or service is genuinely worth. Sustainable profit margins are what keep your business alive long enough to grow.

III. The Marketing Pitfall: Building Something Nobody Finds

A brilliant product that nobody discovers is a business that fails. Many new entrepreneurs underinvest in marketing — either because they lack confidence in it or because they believe the product will sell itself. It will not. Strategic, consistent marketing is what connects your solution to the people who need it.

Build a Strong, Clear Brand Identity

Your brand is more than a logo or a color palette. It is the total perception of your business — what you stand for, how you communicate, and the feeling you create in your audience. Define your mission, your values, and your unique selling proposition (USP) before you build any marketing materials. A clear brand identity makes every touchpoint — your website, social media, emails, and customer interactions — consistent and compelling. It builds trust, and trust builds customers.

Invest in a Multi-Channel Digital Marketing Strategy

If you’re still developing your growth plan, you may also find our guide on income growth strategies helpful for expanding your business sustainably.

In today’s digital-first world, your online presence determines your discoverability. A multi-channel approach ensures you reach your audience wherever they spend time. Effective digital marketing for small businesses includes:

- Search Engine Optimization (SEO): Optimize your website content with relevant keywords so your business appears when potential customers search for what you offer.

- Social Media Marketing: Show up consistently on the platforms where your target audience is active. Engage, educate, and build community.

- Content Marketing: Blog posts, videos, how-to guides, and podcasts that provide genuine value attract organic traffic and establish your authority.

- Email Marketing: Build your email list from day one. It is one of the highest-ROI channels available to small businesses and one you fully own.

Make Customer Service a Competitive Advantage

Word-of-mouth remains one of the most powerful marketing tools available, and it is almost entirely driven by how customers feel after interacting with your business. Respond to inquiries promptly. Resolve issues generously. Follow up after purchases. Actively seek feedback and act on it. A customer who feels valued becomes a repeat buyer and an unpaid brand ambassador. In an era where competitors are a single click away, exceptional service is one of the clearest differentiators you have.

IV. The Operations Pitfall: Working in the Business Instead of On It

Many entrepreneurs start their business to gain freedom but quickly find themselves trapped — working longer hours than any employer would demand, handling every task themselves, and struggling to scale. Operational efficiency and strategic delegation are what separate sustainable businesses from exhausting ones.

Leverage Technology to Streamline Operations

Technology is the small business owner’s great equalizer. The right tools can automate repetitive tasks, improve accuracy, and free up your time for high-value activities. Consider adopting a CRM (Customer Relationship Management) system to manage leads and client relationships, project management tools to keep work organized, accounting software for financial visibility, and automated email platforms for consistent marketing. Every hour saved by the right tool is an hour you can reinvest in growing your business.

Build a Network and Know When to Delegate

No successful entrepreneur builds alone. Surround yourself with mentors who have walked the path before you, peers who challenge your thinking, and professionals — accountants, lawyers, marketers — who fill your skill gaps. As your business grows, resist the instinct to control everything. Strategic delegation — to employees, freelancers, or virtual assistants — allows you to focus on the work that only you can do. Hiring and delegating effectively is not a luxury reserved for large companies; it is a survival strategy for small ones.

Stay Adaptable and Keep Learning

The business landscape evolves constantly — consumer behavior shifts, new competitors emerge, and technologies disrupt established models. Entrepreneurs who thrive long-term are those who commit to continuous learning and remain willing to adapt. Stay informed about industry trends. Experiment with new strategies. Be willing to pivot when the data tells you something is not working. Rigidity is a risk; adaptability is a competitive advantage.

Conclusion

Building a successful small business is not about avoiding all mistakes — it is about avoiding the most costly ones early. Entrepreneurs who invest time in proper planning, manage their finances with discipline, market their business strategically, and build efficient operations dramatically improve their odds of long-term success. The pitfalls covered in this guide are common, but they are not inevitable. Armed with the right knowledge and a commitment to continuous improvement, you can navigate the early challenges of entrepreneurship and build something that lasts.

Key Takeaways

- Start with a realistic business plan and validate your idea before investing heavily.

- Manage cash flow carefully and maintain a financial buffer for unexpected expenses.

- Build a consistent marketing strategy so customers can find and trust your business.

- Use technology and delegation to improve efficiency as your business grows.

- Stay adaptable and continue learning as customer needs and markets evolve.

Frequently Asked Questions

Q1: What is the single most important thing a new entrepreneur can do to avoid failure?

The most impactful step is creating a thorough, realistic business plan before you launch. It forces you to validate your idea, understand your market, plan your finances, and define your path to profitability — reducing costly surprises down the road.

Q2: How much capital do I actually need to start a small business?

This varies significantly by industry, but a reliable rule of thumb is to calculate your startup costs, project your monthly operating expenses, and ensure you have enough runway to cover at least six to twelve months — then add a 20% buffer for the unexpected. Always err on the side of having more capital than you think you need.

Q3: How do I find my first customers?

Start with your existing network — friends, colleagues, and professional contacts. Then use the market research you have done to identify where your target customers gather online and offline. Leverage SEO, social media, and content marketing for organic reach. Offer promotions or referral incentives early on, and prioritize excellent service to generate word-of-mouth from your very first customers.

Q4: What should I do if my business idea is not working?

First, diagnose the problem honestly — is it the product, the pricing, the marketing, or the target audience? Gather feedback from customers and non-customers. Many successful businesses today look quite different from their original concept. Do not be afraid to pivot. The ability to adapt based on real-world feedback is one of the most valuable traits an entrepreneur can develop.

Q5: Should I try to do everything myself at first to save money?

It is natural to handle many tasks yourself early on, but be honest about where your time is best spent. If tasks like bookkeeping, graphic design, or social media are consuming hours you should be spending on sales or product development, outsourcing or hiring part-time help is often the smarter financial decision — not a cost, but an investment in growth.

Disclaimer: This article is for educational purposes only and should not be considered legal, financial, or business advice. Business outcomes vary depending on your industry, market conditions, experience, available resources, and execution. Consider consulting qualified professionals when making important business decisions.