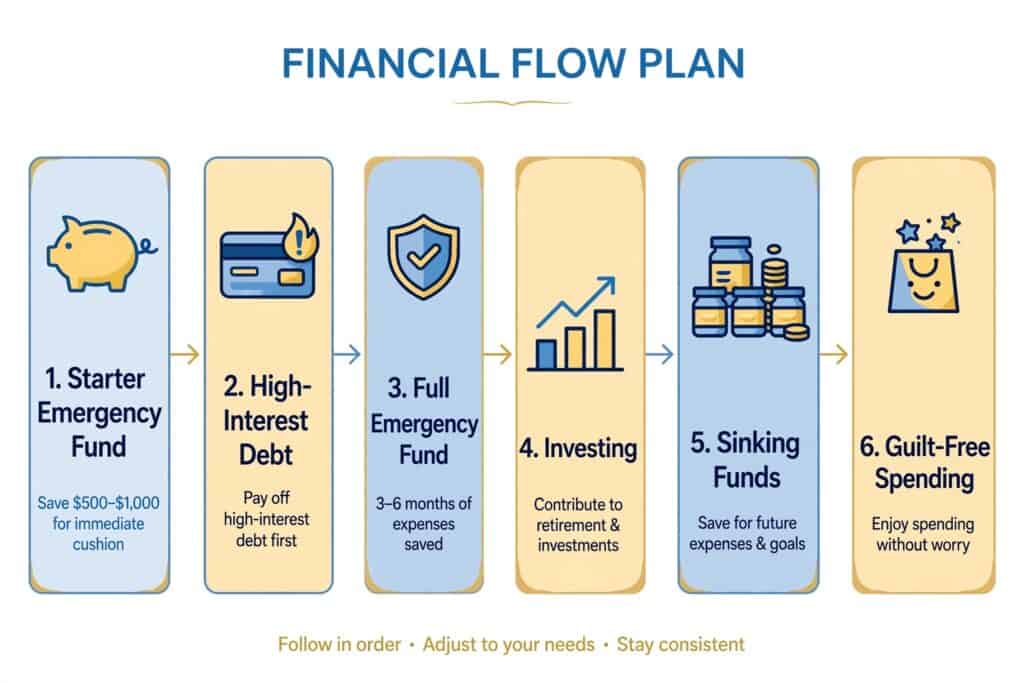

If you’re wondering what to do with leftover money at the end of the month, here’s the short answer: don’t let it sit in your checking account, and don’t spend it on autopilot. Leftover money has 1 job — to move you 1 step closer to financial security. The smartest way to do that is to follow a simple priority order: a $1,000 starter emergency fund first, then high-interest debt, then a full emergency cushion of 3 to 6 months, then investing, and only then guilt-free spending.

That’s the entire strategy in 1 sentence. The rest of this article walks you through each step in plain language, with real numbers, so you know exactly where your extra cash should go — whether it’s $50 or $500.

And if this is the first month you’ve ever had money left over? Congratulations. That surplus is the raw material every wealthy person started with. Let’s make sure it doesn’t slip through your fingers.

For example:

| Priority | Where Your Leftover Money Goes | Why It Comes First |

|---|---|---|

| 1 | Starter Emergency Fund | Protects against unexpected expenses. |

| 2 | High-Interest Debt | Saves money on interest and improves cash flow. |

| 3 | Full Emergency Fund | Creates long-term financial stability. |

| 4 | Investing | Allows your money to grow over time. |

| 5 | Sinking Funds | Prepares for predictable future expenses. |

| 6 | Guilt-Free Spending | Keeps your financial plan sustainable and enjoyable. |

Why Having a Plan for Extra Money Matters

Many people assume that building wealth requires earning a much higher income. While increasing your income certainly helps, what often matters first is learning how to manage the money you already have.

Two people can earn the same salary and end up with completely different financial outcomes. The difference usually isn’t one dramatic financial decision. It’s hundreds of small decisions about where each extra dollar goes.

That’s why having a simple priority system matters. Instead of deciding from scratch every month, you follow the same sequence every time you have money left over.

The result is less stress, fewer impulsive decisions, and steady financial progress over time.

Why Leftover Money Disappears If You Don’t Give It a Job

Here’s something most people learn the hard way: money without a purpose gets spent.

You finish the month with $200 extra in your checking account. You feel good about it. Then a week into the new month, it’s gone — a couple of dinners out, 1 impulse buy, a “small” online order that somehow came to $63. Nothing reckless happened. The money just… evaporated.

That’s not a discipline problem. It’s a structure problem.

The 24-Hour Rule for Surplus Cash

Checking accounts are designed for spending, so money that lives there gets treated as spendable. The fix is simple: the moment you notice leftover money, move it somewhere with a name and a purpose — ideally within 24 hours, before everyday spending quietly absorbs it.

Where exactly should it go? That depends on where you are in the 6 steps below. Find your step, and send the money there.

Start With the Foundation

Every strong financial plan is built in layers. Trying to invest before building emergency savings or eliminating expensive debt is a bit like building the roof before the walls. Each step in this guide prepares you for the next one.

Although it may feel slower than chasing quick returns, a strong financial foundation usually produces better long-term results.

Step 1: Build a $1,000 Starter Emergency Fund First

If you don’t have at least $1,000 sitting in a separate savings account, every dollar of leftover money goes here first. No exceptions, no skipping ahead.

Why $1,000 Comes Before Everything — Even Debt

It might feel strange to save while you’re carrying a credit card balance. But without a cash buffer, the next surprise expense — a car repair, a vet bill, a cracked phone screen — goes straight onto that same credit card, and you end up borrowing your way backward faster than you’re paying your way forward.

$1,000 won’t cover a true catastrophe, but it absorbs roughly 80% of the everyday surprises that knock people off track.

A Real-World Example

Maya ends most months with about $150 left over. Instead of letting it sit, she transfers it to a savings account labelled “Emergency Only” the same day she notices it. In just under 7 months, she has her full $1,000 buffer — and for the first time in her adult life, a flat tire is an inconvenience, not a crisis.

If you want to speed this step up by creating a bigger monthly surplus in the first place, our guide to 10 money saving habits that actually work covers the exact habits that free up that extra cash.

Step 2: Attack High-Interest Debt (Anything Above Roughly 8%)

Once your starter fund exists, leftover money should go after expensive debt — credit cards, payday loans, and high-interest financing. This is the highest guaranteed return available to you anywhere.

The Math That Makes This a No-Brainer

Paying off a credit card with a 21% annual interest rate effectively avoids paying that same interest in future borrowing costs. While it’s not an investment return, reducing high-interest debt is often one of the most effective ways to improve your overall financial position.

A Real-World Example

Jordan carries a $2,400 credit card balance at 21% interest and pays the $70 minimum each month. By redirecting his $200 of monthly leftover money on top of that minimum, he clears the entire card in about 10 months instead of dragging it out for years — and saves several hundred dollars in interest along the way.

Avalanche vs. Snowball: Pick 1 and Commit

| Method | How It Works | Best For |

|---|---|---|

| Avalanche | Pay extra on the highest interest rate first | Saving the most money overall |

| Snowball | Pay extra on the smallest balance first | Motivation through quick wins |

Both methods work. The right one is whichever you’ll actually stick with for the next 6 to 18 months.

One note: lower-interest debt — like a mortgage or a car loan under roughly 8% — can usually wait. Your leftover money tends to do more for you in the next steps. If debt has been a long-running source of stress for you, our guide Stop Struggling With Money walks through rebuilding your finances from the ground up.

Step 3: Grow Your Emergency Fund to 3–6 Months of Expenses

With the expensive debt gone, return to your emergency fund and build it from $1,000 up to 3 to 6 months of essential expenses.

How to Calculate Your Target Number

Add up only your must-pay monthly bills: rent or mortgage, groceries, utilities, transport, insurance, and minimum debt payments. If that total is $2,500 a month, your full emergency fund target is $7,500 to $15,000.

That sounds enormous — but remember, you’re now free of high-interest payments, so the money that used to go to interest gets redirected here. Keep it in a high-yield savings account so it earns interest while it waits, but stays accessible within a day or 2.

3 Months or 6? A Simple Rule of Thumb

- 3 months if your income is stable and your household has 2 earners

- 6 months if you’re self-employed, on commission, or a single-income household

This cushion is what separates people who stay financially secure from people who keep starting over every time life throws a punch. We go deeper on this stage in our simple roadmap to building lasting wealth.

Step 4: Start Investing Your Leftover Money

This is where leftover money stops protecting you and starts growing you.

Once the safety layers are in place, extra money at the end of the month should flow into investments — broad index funds, registered retirement accounts (a TFSA or RRSP in Canada, a 401(k) or Roth IRA in the US), or a simple brokerage account with automatic monthly contributions.

What $200 a Month Can Actually Become

Historically, broadly diversified stock market portfolios have produced positive long-term returns, although yearly performance varies and future returns are never guaranteed. Financial research from organizations such as Vanguard and Morningstar consistently emphasizes that long-term investing and diversification have historically been important factors in building wealth over time.

Using a hypothetical average annual return of 8% for illustration only, investing $200 each month could grow to approximately:

- $14,700 in 5 years

- $36,600 in 10 years

- $118,500 in 20 years

That last figure is not a typo. It’s what happens when small, consistent amounts of money get decades to compound. Past performance never guarantees future results — but the principle of compounding has built more quiet wealth than any get-rich-quick scheme ever has.

You Don’t Need Thousands to Start

Fractional shares mean you can begin with whatever this month’s leftover happens to be — even $25. Our beginner’s roadmap to investing with $100 shows you exactly how to open an account and make your first investment this week.

Further Reading

Readers interested in learning more about long-term investing can explore educational resources from:

- Vanguard Investor Education

- Morningstar Investing Classroom

- Financial Consumer Agency of Canada

- Consumer Financial Protection Bureau (U.S.)

Step 5: Fund Your Sinking Funds (The Anti-Surprise Strategy)

Some expenses aren’t emergencies — they’re just irregular. Christmas. Car insurance renewals. A friend’s wedding. That annual software subscription you forget about every single year.

These predictable-but-unbudgeted costs wreck more budgets than genuine emergencies do.

Planning Ahead Reduces Financial Stress

One reason sinking funds are so effective is that they transform predictable expenses into manageable monthly savings goals. Instead of scrambling to pay a large annual bill, you’ve already prepared for it little by little throughout the year.

This reduces financial surprises and makes your monthly budget much more predictable. Financial confidence often comes from preparation rather than income alone.

How a Sinking Fund Works

A sinking fund is a small, named savings bucket you drip leftover money into ahead of time. You’re essentially paying December’s bills in March, in tiny instalments, so they never land as a lump-sum shock.

Example: You know the holiday season costs you about $600 extra. Putting $50 of leftover money into a “Holidays” bucket each month starting in January means December arrives fully paid for — and January arrives without a credit card hangover.

4 Sinking Funds Worth Starting Today

- Car maintenance and repairs — $40 to $75 per month

- Gifts and holidays — $30 to $50 per month

- Annual bills and subscriptions — total your yearly bills, divide by 12

- Travel — whatever your next trip costs, divided by the months until you go

Step 6: Spend Some of It — On Purpose

Here’s the part most personal finance articles skip: if every leftover dollar disappears into responsible buckets forever, you’ll eventually rebel against your own plan. Humans don’t stick with systems that feel like punishment.

So once steps 1 through 5 are running, deliberately assign a slice — say 10% to 20% of your leftover money — to completely guilt-free spending.

The keyword is deliberately. Spending $40 on something you genuinely enjoy, on purpose, is a healthy budget working as designed. Watching $200 vanish without a single conscious decision is a leak. Same money, completely different outcome.

Remember That Income and Spending Work Together

Building wealth isn’t only about spending less. Nor is it only about earning more. The strongest financial plans usually combine both. Reducing unnecessary expenses creates an immediate surplus.Increasing your income expands that surplus even further.

Together, those two habits create more opportunities to save, invest, and build long-term financial security.

Bonus: Grow the Leftover Itself

There’s a second lever most people never pull: instead of only optimizing the surplus, increase it.

Cutting expenses has a floor — you can only trim so far. Income has no ceiling. Every extra $100 you earn per month is $100 more flowing through the 6-step priority list above, and it compounds the same way.

If you already work full-time, our guide to realistic digital income ideas for full-time employees breaks down side income streams you can build in evenings and weekends without quitting your job. Pairing a bigger surplus with this priority system is exactly the combination we explore in Financial Freedom: The Hidden Truths You Must Know Now.

Quick Recap: Where Should Leftover Money Go?

- $1,000 starter emergency fund — your buffer against everyday surprises

- High-interest debt — the highest guaranteed return you’ll ever get

- Full emergency fund (3–6 months) — your sleep-at-night money

- Investments — where compounding quietly takes over

- Sinking funds — for predictable irregular costs

- Guilt-free spending — a fixed slice, chosen on purpose

Find where you currently sit on this list, and send this month’s leftover money there. Next month, do it again. That’s the entire system — boring, repeatable, and remarkably effective.

Final Thoughts

One of the simplest financial habits you can develop is deciding where every extra dollar will go before you have the chance to spend it. Whether your leftover money is $25, $100, or $500 this month, the priority order remains exactly the same.

Build your emergency fund.

Eliminate expensive debt.

Strengthen your financial safety net.

Invest consistently.

Prepare for future expenses.

And finally, enjoy some of your progress without guilt.

The amounts will change over time. The system doesn’t have to. Small, consistent financial decisions repeated month after month often accomplish far more than occasional bursts of motivation.

Frequently Asked Questions

Should I save or invest leftover money?

Save first, invest second. Until you have $1,000 set aside and no high-interest debt, saving wins because it protects you from going backward. After that, investing wins, because long-term compounding beats savings account interest.

Is it bad to leave extra money in my checking account?

It’s not dangerous, but it’s wasteful. Checking accounts pay little or no interest, and money sitting there tends to get spent without a decision. Move it to a named account within 24 to 48 hours of noticing it.

What should I do with $100 left over at the end of the month?

Follow the exact same priority order — the amounts change, the order doesn’t. $100 a month is $1,200 a year, which is a complete starter emergency fund, a serious dent in a credit card balance, or the foundation of an investment portfolio.

How much leftover money should I have each month?

A healthy long-term target is around 20% of take-home pay going toward savings, debt payoff, and investing combined. If you’re nowhere near that yet, don’t panic — start with whatever is left over this month and grow it gradually with better habits and extra income.

Should I follow these steps if I live in Canada?

The overall order—building emergency savings, paying off high-interest debt, investing, and preparing for future expenses—applies broadly. However, the accounts and tax advantages available to you may differ depending on where you live. For example, Canadians may use TFSAs or RRSPs, while U.S. investors often use 401(k)s or Roth IRAs.

Final disclaimer

This article is provided for educational purposes only and does not constitute financial, investment, tax, or legal advice. Financial situations vary from person to person. Before making significant financial decisions, consider consulting a qualified financial professional who can provide advice based on your individual circumstances

Related Reading on PBroad2Riches: